Blog

SBA vs. Traditional Lending for Dentists: Which Loan Fits the Need?

Most dental practices hit a point where growth takes more cash than the business has.

For an associate dentist, that might mean buying a practice and stepping into ownership. For an existing owner, it could mean adding operatories, replacing equipment, buying the building, refinancing debt, or bringing on a partner. Sometimes the need is more day-to-day, like covering working capital during a remodel, smoothing out cash flow, or investing in technology the team has been putting off.

All of those decisions touch the practice’s finances.

New equipment may help with diagnostics, patient experience, or speed, but the payment still has to work inside the monthly cash flow. A remodel may create more room for production, but it can also slow the schedule while the work is happening. A practice acquisition may be the right move for ownership, but the buyer still needs enough cash left after closing to run the practice without feeling squeezed.

That is where the loan structure starts to matter.

Dentists usually hear financing talked about in two buckets: SBA loans and traditional bank loans. That is a useful starting point, but the label alone does not tell you much.

A practice purchase, equipment upgrade, building purchase, refinance, remodel, expansion, or working capital need may each call for a different setup. The better question is what the money is being used for, how soon it is needed, and whether the payments leave the practice with enough room to operate.

SBA and traditional loans can both make sense in dental practice financing. The fit depends on the job.

SBA vs. Traditional Lending: What is the Difference?

SBA lending adds a government guarantee to a bank-funded loan. Traditional lending does not.

That guarantee can give the lender more flexibility when a project is strong but does not fit neatly into conventional lending. Traditional loans rely on the bank’s internal credit standards, collateral requirements, and underwriting.

For a simple equipment purchase, a conventional loan may be the cleaner fit. For more layered projects, like buying a practice, refinancing debt, funding a remodel, or covering working capital, SBA financing may make more sense.

One option is not automatically better than the other. They solve different problems.

Why SBA Financing Matters in Dental Lending

SBA financing matters in dental lending because many dental deals are built around cash flow, not just hard collateral.

A practice acquisition often includes goodwill, patient records, equipment, working capital, and transition costs. Not all of that is easy to secure with collateral, but it can still be part of a strong deal. A first-time buyer may be ready for ownership but needs to preserve cash after closing. An established owner may have strong revenue but still need room for payroll, supplies, lab fees, marketing, or growth.

That is where SBA financing can be useful. It can give the loan structure more room to account for the full project, not just the easiest piece to finance. In some cases, that may mean longer repayment terms, lower down payment potential, more flexible use of funds, or support when collateral is limited.

For a dentist, that structure can matter as much as the loan amount. The goal is not just to get the deal closed. It is to make sure the practice has enough room to operate after the loan is in place.

Why Traditional Lending Still Matters

Traditional lending still matters because not every project needs added flexibility of SBA financing.

For a simple equipment purchase, a contained office update, a straightforward building purchase, or short-term working capital need, a conventional loan may be the cleaner fit.

It can work well when the borrower has strong credit, solid liquidity, stable practice performance, and a clear use of funds. Depending on the deal, it may also mean a simpler process, less paperwork, or a faster path.

Traditional lending is not the opposite of SBA lending. It is a different structure. When the project is straightforward, it may be the cleanest answer.

The SBA Loans Dentists are Most Likely to Hear About

Dentists do not need to know every SBA rule before talking with a lender, but two programs come up often in practice financing: SBA 7(a) and SBA 504.

SBA 7(a) is usually the more flexible option. In dental lending, it is often used for practice acquisitions, working capital, partner buyouts, ownership changes, certain refinances, or projects with several uses of funds. That makes it a common fit for practice purchases, where the loan may need to cover goodwill, equipment, transition costs, and working capital together.

SBA 504 is more focused on major fixed assets. For dentists, this means owner-occupied commercial real estate, major equipment, or larger fixed-asset projects. A dentist buying the building where the practice operates may look at SBA 504 alongside conventional commercial real estate financing.

The simplest distinction is this: 7(a) is often used when the project needs flexibility, while 504 is used when the project is tied to a major fixed asset, like the practice building.

What Traditional Lending Can Look like for Dentists

Traditional lending is not one single product. It can show up in a few different ways, depending on the need.

A term loan can work well when the project is defined, and the practice needs a lump sum of capital. That could be a remodel, office refresh, technology upgrade, or an improvement project.

An equipment loan is usually tied to a specific purchase, such as a CBCT system, intraoral scanner, dental chairs, sterilization equipment, or other major clinical tools. Since the asset is clear, the financing can often be matched to the useful life of the equipment.

A line of credit serves a different purpose. It is usually better for timing gaps and short-term working capital needs. That may include vendor timing, uneven expenses, temporary cash pressure, or disruption during a project.

Conventional commercial real estate financing may fit when the main need is buying, refinancing, or improving property. For a strong borrower with a clean building purchase, a traditional real estate loan may be the most direct option.

The broader point is that traditional lending gives dentists several paths. The fit depends on what is being financed, how clear the project is, and how the repayment needs to line up with practice cash flow.

The Mistake Dentists Make When Choosing a Loan

One of the biggest mistakes dentists make is choosing by loan label instead of use of funds.

It is easy to focus on the rate, approval amount, or whether the loan is SBA or conventional. Those details matter, but they do not tell the whole story.

A low rate can still create pressure if the payment does not fit the practice’s cash flow. A fast approval may not solve the full need. A larger loan amount may not help if the structure does not match the project. An equipment loan may be perfect for one purchase, but not for a larger acquisition or expansion.

The better questions are more practical: What is the practice financing? Is the need short-term or long-term? Is it one asset or several uses of funds? Does the project need flexibility, speed, or simplicity? Will the practice still have enough working capital after closing?

Those questions shift the conversation from which loan sounds better to which structure actually supports the practice.

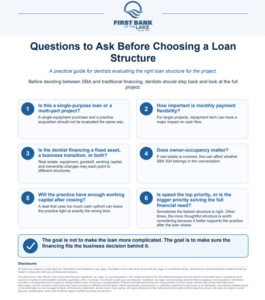

Questions to Ask Before Choosing SBA or Traditional Lending

First_Bank_of_the_Lake_Loan_Structure_Questions_One_Page_Fixed_Logo

Why Lender Guidance Matters

Lenders may look at the same dental project differently.

One lender may focus more heavily on collateral. Another may put more weight on cash flow. One may see the request as a conventional loan. Another may see where SBA financing could make the structure work better.

Even with SBA loans, lenders can vary in how they think about risk, structure the financing, and guide the borrower through the process.

That is why the lending conversation matters.

A good lender should help the dentist understand the tradeoffs. What does SBA financing help solve? What does conventional lending keep simpler? How does the monthly payment affect cash flow? How much working capital remains after closing? What happens if the project takes longer or costs more than expected? First Bank of the Lake is happy to discuss these questions and any others that you have as you consider your funding options.

Ultimately, the decision is bigger than SBA versus traditional lending. It is also about working with someone who can explain the options clearly and match the structure to the actual need.

For dentists, that kind of guidance can make the financing decision feel less confusing and more connected to the practice’s next step.

Final Thoughts

SBA and traditional lending can both make sense for dental practices. The right fit depends on the project, the borrower, the practice, and how much flexibility the structure needs.

A better question than “Should I use SBA or conventional financing?” is: “What structure fits this project, this practice, and this stage of ownership?”

That usually leads to a better lending conversation, and a financing decision that still works once the loan is closed.

Special Thanks

DrillDown thanks First Bank of the Lake for contributing this guest article and sharing its SBA lending perspective with our dental practice audience. At First Bank of the Lake, SBA lending is a focused part of the team’s work, combining SBA experience, practical guidance, and a relationship-driven approach to help business owners explore financing options that fit their goals. Their team works to make the lending process clearer, with early expectations, steady communication, and support from the first conversation through closing.

First Bank of the Lake (“Bank”) does not provide financial, investment, tax, legal, or accounting advice. The content provided is for informational purposes only and should not be relied upon or considered as an express or implied recommendation, warranty, guarantee, offer, or promise. You should consult your own financial, investment, tax, legal, and accounting advisors before engaging in any transaction

![]()

Note: The material and contents provided in this article are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.