Blog

Why is my distribution being taxed as Capital Gains?!

If you’re a shareholder in an S Corporation, you might be surprised—or frustrated—to find out that a distribution you thought was tax-free is now showing up as capital gains on your tax return. What’s going on?

Let’s break it down.

The Issue: Basis Determines Taxability

In most cases, distributions from an S Corporation to a shareholder are not taxable, as long as you have enough basis. But if your basis is too low, any distribution in excess of basis becomes taxable—and is treated as a capital gain.

Tax Basis 101: What Increases and Decreases It

Your stock basis goes up when:

You contribute capital

The company generates profits (taxed to you via pass-through)

It goes down when:

You take distributions

The company has losses

There are noncash deductions—like depreciation

The Common Culprit: Depreciation

Depreciation is a noncash expense that reduces net income—and therefore your basis—even though no money has actually left the business. And if the equipment was 100% financed, the business still has the cash on hand to distribute.

That cash might be tempting to take—but if your basis has been reduced by depreciation, you could wind up with a distribution in excess of basis and an unexpected capital gains tax bill.

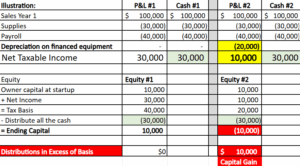

Let’s Look at a Simple Example

Scenario:

You buy a $100,000 piece of equipment

It’s fully financed (no out-of-pocket cash used)

You take $20,000 of depreciation

The depreciation lowers net income, which lowers your basis—but the business still has cash (since the equipment was financed). If you then take a distribution using that cash, you may exceed your tax basis.

Result: That distribution—despite being from cash you think you “earned”—may be partially or fully taxable as a capital gain.

Illustration of Distributions in Excess of Basis

Key Takeaway

Before taking distributions, always ask:

“Do I have enough basis to cover this?”

Distributions beyond your basis trigger capital gains tax, and it’s often depreciation (especially on financed equipment) that quietly chips away at your equity and sets you up for this surprise.

Need help tracking basis and planning distributions wisely?

Contact DrillDown Solution and avoid the capital gains curveball: Contact Us – Drilldown Solution – ACT

Note: The material and contents provided in this article are informative in nature only. It is not intended to be advice and you should not act specifically on the basis of this information alone. If expert assistance is required, professional advice should be obtained.